Regulating in the Shadows: How Agencies Achieve Indirectly that Which they have No Authority to Achieve Directly

When is it appropriate for a government agency to use its powers and force citizens to give up legal rights in order to achieve the agency’s goals? When does this power become overly coercive? The authors of this paper delve into these important questions.

Contributors

John Allison

James “Jimmy” Conde

Charles “Chuck” Cooper

C. Boyden Gray

Adam Gustafson

Michael Kelly

Cleta Mitchell

George J. Terwilliger, III

This paper was the work of multiple authors. No assumption should be made that any or all of the views expressed are held by any individual author. In addition, the views expressed are those of the authors in their personal capacities and not in their official/professional capacities.

To cite this paper: J. Allison, et al., “Regulating in the Shadows: How Agencies Achieve Indirectly that Which they have No Authority to Achieve Directly”, released by the Regulatory Transparency Project of the Federalist Society, July 5, 2017 (https://rtp.fedsoc.org/wp-content/uploads/RTP-Enforcement-Agency-Coercion-Working-Group-Paper.pdf).

Introduction

Agencies throughout the federal government have a vast array of powerful administrative remedies at their disposal to achieve their policy goals. These powers can be used to place great pressure on companies and individuals to surrender their rights and to submit to the government’s policy preferences. When is it appropriate for a government agency to use these powers and force citizens to give up legal rights in order to achieve the agency’s goals? When does this power become overly coercive?

This paper is designed to explore agency coercion and to describe examples where agencies have gone too far in wielding these administrative powers. There are important rights at stake, including constitutional rights. For instance, some coercive agency powers can force businesses to surrender important constitutional rights – such as the right to contest criminal charges in front of an impartial jury. Other powers can compel people to defend themselves in administrative forums without the rights they would receive in the court system. In other situations, officials can use the threat of regulation to impose government policy preferences on businesses and individuals without their consent and without any oversight by Congress. Finally, some of these powers allow the government to cut businesses off from basic services – such as the right to hold accounts at financial institutions – simply because some government officials do not like how the business is conducted.

This problem may seem counterintuitive. The federal government is – and should be – limited in its ability to act by the Constitution, principles of federalism, and the laws enacted by Congress. The federal government cannot disregard these constraints and impose its will on the American people simply because those constraints are burdensome and inconvenient.

But these administrative powers often allow agencies to achieve indirectly what they cannot achieve directly. And these powers are often wielded outside of public view and without significant public scrutiny as to whether they are being used appropriately. For instance, if a company depends on federal contracts, the government can force a company to pay substantial financial penalties – even if the company believes it did nothing wrong – by threatening to exclude the company from participating in any federal contracts or programs and thereby putting the company’s financial health in jeopardy. Similarly, the government can threaten to make wide and far-reaching adverse regulatory decisions against companies and their employees if they do not succumb to the government’s policy wishes. For instance, if a financial institution were to reject a request from the government to change its behavior, it may find that its federal regulator will deny all future applications to expand its business. These types of practical powers help government officials to obtain results that are not required under any law or regulation and that can force companies and individuals to surrender important rights and freedoms without any legitimate justification and without significant oversight by Congress or the courts.

This problem is not a partisan issue. Both Democratic and Republican Administrations can succumb to the temptation to use these coercive powers in inappropriate ways to achieve their policy goals. When government officials have broad power at their disposal, it can be easy to lose one’s way and to use that power in intemperate ways. Only a vigilant and informed public can ensure that government officials are operating based on principle and not simple expediency.

Throughout this paper, we have highlighted some examples where the federal government has been able to use powerful administrative remedies to coerce companies and individuals into surrendering important rights or freedom without any good reason and without any independent oversight. These kinds of inappropriate coercion should concern everyone, regardless of which political party is in power.

I. The Unfairness Posed By the Increased Use of SEC Administrative Proceedings

In many federal investigations, a government agency can bring a legal action against a company or individual only in federal district court. However, some agencies, like the Securities and Exchange Commission (“SEC” or “the Commission”), have a powerful alternative: they can bring administrative proceedings, which are presided over by their own administrative law judges and not independent federal district judges. By sidestepping federal district court, the SEC can put nearly any company or individual at a distinct disadvantage, depriving them of significant rights and increasing its own chances of success.

This was not always the case. Before the Dodd-Frank Act was passed in 2010, the SEC could file an administrative complaint and recover money only from companies and individuals who were registered in some capacity with the SEC (such as investment advisors). If the SEC wanted to recover a monetary fine from a non-regulated company or individual, then it had to file a lawsuit in federal district court.1 But Congress changed that with Section 929P of the Dodd-Frank Act.2 Now, the SEC can recover monetary penalties from nearly anyone in administrative proceedings for violations of securities laws.

With the change in the law, the SEC has shifted away from the courts and toward administrative proceedings. The SEC has generally filed fewer settlements in court, where they could be scrutinized by federal judges.3 And the SEC has generally won a much higher percentage of contested cases in its administrative forum than it has in federal courts. For instance, from September 2013 through September 2014, “the SEC won 100% of its contested administrative hearings, but only 61% of trials held in federal court.”4

These different rates of success are not surprising because the SEC enjoys several important advantages in administrative proceedings that it does not have in federal court. For example, neither the Federal Rules of Civil Procedure nor the Federal Rules of Evidence apply in administrative proceedings.5 Rather, the proceedings have been governed by the SEC’s Rules of Practice, which historically provided for more limited discovery (such as the taking of depositions only at the SEC’s discretion).6 Without the Federal Rules of Evidence, the SEC can use hearsay to prove its case against a party in a way that it cannot in federal court. There is also no right to a jury trial in administrative proceedings, and decisions rendered in SEC administrative hearings are given substantial deference by federal appellate courts.7

The SEC has responded to concerns about its administrative proceedings by adopting amendments to its Rules of Practice.8 These amendments, among other things, lengthen time periods for administrative law judges to make some of their rulings, permit a small number of depositions for each side, permit additional dispositive motions, and would only permit hearsay if it is relevant, material, and reliable. While these new rules are an improvement over the old practice, the basic problems still remain, and defendants are still at a distinct disadvantage in administrative hearings.

Moreover, the amendments do not address the most controversial advantage the SEC enjoys in administrative proceedings: the use of its own administrative law judges. When the SEC institutes administrative proceedings against a company or individual, the SEC presides over the action but “it typically delegates review to an Administrative Law Judge.”9 If the administrative law judge decides in favor of the Commission, then the party may appeal the decision to the Commission itself and then to a federal appellate court. Federal district courts are not involved in this process.

Litigants are starting to make constitutional challenges to the SEC’s use of administrative law judges. Between 2015 and 2016, four federal appellate courts rejected constitutional challenges to the use of ALJs on technical grounds. See Tilton v. Sec. and Exch. Comm’n, 824 F.3d 276 (2d Cir. 2016); Hill v. Sec. and Exch. Comm’n, 825 F.3d 1236 (11th Cir. 2016); Jarkesy v. Sec. and Exch. Comm’n, 803 F.3d 9 (D.C. Cir. 2015); Bebo v. Sec. and Exc.e Comm’n, 799 F.3d 765 (7th Cir. 2015). In each case, the SEC had instituted an administrative proceeding against a party, which responded by filing a separate constitutional challenge in federal district court. The appellate courts held that the district courts did not have jurisdiction to decide whether the use of ALJs was constitutional in these circumstances, and that the party had to pursue their constitutional challenges through the SEC administrative process before appealing to federal appellate courts.

However, as some cases are now winding their way through the SEC’s administrative process, courts are now beginning to decide this question on the merits. In December 2016, the Tenth Circuit held that the use of SEC administrative law judges are unconstitutional because they were employees and were “not appointed by the President, a court of law, or a department head” as the Constitution’s Appointment Clause requires.10 Rather, “the [Office of Personnel Management] screens applicants, proposes three finalists to the SEC, and then leaves it to somebody at the agency to pick one.”11 The Tenth Circuit found that, under the current process, the SEC is not permitted to: (1) hire administrative law judges in such a diffuse manner (where it was unclear who at the agency is responsible for the hiring); (2) delegate cases to those judges; and (3) litigate the cases in front of them.12 This constitutional issue will undoubtedly be decided by the Supreme Court in the next few years.

In the meantime, the substantial advantages enjoyed by the SEC – restricted discovery, freedom to use hearsay, no right to a jury, limited appellate rights, and its own administrative law judges – provide the SEC with substantial power in administrative proceedings, particularly in settlement negotiations. The administrative process provides a more-friendly forum for the SEC to litigate cases where it might have a tenuous legal theory. Similarly, the limitations of SEC administrative hearings may prevent companies and individuals from fully presenting their defenses, thereby causing them to settle cases that they may not have settled as easily (or for as much money) in federal court. As one federal judge has acknowledged, the SEC’s increased leverage in administrative proceedings can “present serious problems for those defending such actions.”13

Officials from the SEC have argued that administrative proceedings result in faster decisions and are heard by “specialized factfinders,” that administrative law judges can consider relevant evidence, and that some types of actions (such as those relating to failure to supervise) can only be brought in an administrative setting.14

But those arguments ignore the fundamental lack of fairness that results when one party is able to choose the forum, the judges, and the rules that govern the proceedings. The SEC should not have the ability to impose monetary penalties on nearly any citizen with only limited oversight from an independent federal judiciary. Nor should the SEC be able to write the rules governing those proceedings in which it has a financial interest. The SEC administrative proceedings may be faster, but they are not fairer. It is this basic unfairness at the heart of SEC administrative proceedings that should be addressed and fixed.

Related reading

II. The Use of Debarment as a Threat to Influence Legal Proceedings

Debarment and suspension are powerful tools that the government can unfairly use to coerce a company into surrendering its rights and changing its business practices without any substantial judicial involvement. If a company is debarred, it is generally not allowed to participate in any federal contracts for a set period of time. A suspension is a temporary measure with the same effect. Because even the threat of debarment and suspension can be devastating to companies and individuals dependent on receiving work or compensation from the federal government, the United States can use that threat as a way to influence the outcome of criminal investigations, civil lawsuits, and even administrative audits. In many cases, the threat is so powerful that the government need not raise it overtly in order to achieve the results that it wants.

If the federal government determines that a company or individual is not presently responsible, the federal government can debar a company for up to three years, leaving the company ineligible for any contracts with the federal government.15 It can also temporarily suspend a company from participating in federal contracts pending debarment proceedings. Contractors can be debarred pursuant to either a federal statute or the Federal Acquisition Regulation. Among other things, a company can be debarred for a criminal conviction or a civil judgment indicating a lack of business integrity or business honesty that seriously and directly affects the present responsibility of a government contractor or subcontractor.16 Although debarment is designed to protect the public and the government from irresponsible contractors, rather than to punish those contractors, the consequences can still be devastating.17 Not only does debarment result in loss of contracts government-wide, it also inflicts reputational damage and can endanger a company’s ability to stay afloat until the end of the debarment period.18 For these reasons, debarment is often described as the corporate death penalty.

A. How Debarment and Suspension Can Affect Criminal Cases

A North Carolina hospital system showed how debarment can play a significant role in resolving a criminal case. In 2012, the government accused WakeMed, the largest hospital system in eastern North Carolina, of billing for overnight hospital stays for patients when a physician had not ordered it or had ordered the discharge of the patient.19 “Though some WakeMed managers were aware of the billing practices, according to court documents, investigators found no evidence of anyone personally benefiting from the system.”20 After an external audit raised concerns about the practice, and prior to any criminal investigation, WakeMed conducted its own review and offered $1.4 million in refunds to Medicare.21 Medicare accepted $1.2 million of that offer.22 Prior to any criminal investigation, WakeMed also made substantial improvements to its compliance program.23

Despite WakeMed’s efforts, the federal government began a criminal investigation and ultimately decided that it wanted to impose criminal and civil penalties on WakeMed.24 The government eventually offered to settle its criminal investigation and enter into a deferred prosecution agreement with WakeMed in exchange for $8 million in penalties.25 These penalties were extrapolated based on a random sample of bills that the government selected for review.26 Under the government’s proposal, WakeMed was also required to enter into a corporate integrity agreement (including an outside monitor which would report its findings to the government), to cooperate with the government in its investigation, and to promise not to dispute the agreed statement of facts.27 On the same day that the agreement was finalized, WakeMed’s chief executive officer told reporters that he did not believe criminal charges were warranted and that none of the employees had knowingly done anything wrong.28

But WakeMed had no choice but to enter into the deferred prosecution agreement. An indictment could potentially jeopardize the hospital’s ability to operate as a going concern. The mere existence of an indictment could also lead to the hospital’s suspension from the Medicare program and ultimately a debarment from the Medicare program if it were convicted. No hospital could risk that possibility. In approving the deferred prosecution agreement, a federal district judge highlighted the potential consequences from a criminal charge, observing that its consideration must also include, however, the protection of defendant’s employees and healthcare providers who are blameless but who would suffer severe consequences should defendant be convicted and debarred as a Medicare and Medicaid provider. Moreover, the Court has considered the threat that the provision of essential healthcare to WakeMed’s patients would be interrupted and that the needs of the underprivileged in the surrounding area would be drastically and inhumanely curtailed should defendant be forced to close its doors as a result of the instant prosecution.29

Because the United States promised that WakeMed would not be debarred from Medicare if it agreed to the government’s proposal,30 WakeMed signed the deferred prosecution agreement. Regardless of whether WakeMed had a viable defense, it had no choice but to sign the agreement. The threat of debarment explained the hospital’s capitulation even where the CEO believed the company was innocent of any criminal offense.

B. How Debarment and Suspension Can Affect Civil Cases

The threat of debarment is used to achieve the same effect in civil cases. In November 2016, one of the country’s largest construction and engineering companies (with over 50,000 employees), Bechtel National, Inc. (“Bechtel”), and its subcontractor agreed to pay $125 million to settle a federal lawsuit under the False Claims Act. The lawsuit, originally filed in 2013, alleged that Bechtel performed work under a contract with the Department of Energy that did not meet the required standards for quality or safety.31 This particular project involved the design and building of a waste treatment plant at Hanford Nuclear Site in Washington, which for decades housed plutonium for nuclear weapons.32 The relators alleged, among other things, that Bechtel knowingly performed testing using inadequate simulants in order to save money,33 and utilized prohibited methodologies in developing safety control measures.34 Just three weeks after the government notified the Court that it would partially intervene in the case, the parties entered into a settlement. By doing so, Bechtel did not admit any liability or wrongdoing, and stated that the company “take[s] our responsibilities as a government contractor very seriously . . . .”35

By settling the case, Bechtel took action to avoid the costs and “distraction”36 of a trial, but it also took major steps to lessen the danger of debarment. While it is argued that that some companies are too big to debar, it nevertheless remains a possible consequence that is simply too damaging to risk by taking a case to trial. Without the ever-looming concern of debarment, Bechtel may have chosen to assert defenses that its actions did meet the standards for nuclear waste treatment. Indeed, the company expressly denied the allegations in the complaint and stated that the Hanford project is “the most challenging and complex radioactive waste problem in U.S. history.”37 Despite denying the allegations publicly, Bechtel (as one of the largest federal prime contractors in the nation) had substantial incentive to settle the case, continue performing on its contract, and not risk any potential additional consequences that could arise from debarment.

C. How Debarment and Suspension Can Affect Responses to Administrative Audits

Finally, the threat of debarment can raise its head in administrative disputes. For instance, in one recent high profile administrative proceeding, Palantir Technologies (“Palantir”) was threatened with debarment by the Labor Department, which complained that Palantir discriminated against Asian applicants for software engineering positions.38 The Labor Department also asserted that Palantir was relying on a hiring system that relied on recommendations from existing employees.39 To put additional pressure on Palantir, the Labor Department sought the cancellation of all of Palantir’s existing contracts with the federal government and to debar the company from future contracts.40 The company denied the allegations, but ultimately settled the complaint for more than $1.6 million while continuing to deny the allegations.41 Palantir contested this complaint longer than most companies would have. The government was able to use the threat of debarment to persuade Palantir to settle, and it did not ultimately matter if Palantir had a meritorious defense to the charges.

D. Conclusion

Even though the federal government and its contractors may not explicitly discuss the risk of debarment during the course of an investigation or lawsuit, it is often the government’s most powerful tool in reaching a settlement with a contractor. Both sides know that debarment is a potentially crippling possibility in the event of a criminal conviction or civil judgment. Although settling criminal or civil allegations does not provide immunity from debarment, a settlement without any admission of wrongdoing lessens the possibility of debarment. The mere threat of debarment may induce companies to settle even if the company believes it would have a defensible and strong position during litigation.

In many cases, the threat is so powerful that the government need not raise it overtly in order to achieve the results that it wants.

Receive more great content like this

III. Operation Choke Point

Offering short-term or “payday” loans, selling firearms and ammunition to lawful purchasers, and coin dealing are perfectly legitimate and lawful businesses. Beginning in 2011, however, several federal agencies have colluded in a backroom effort—which the agencies themselves dubbed “Operation Choke Point”—designed to eliminate entire industries without passing a law against them or bringing a prosecution against the companies that engage in them. According to an investigative report by a congressional oversight committee, Operation Choke Point proceeded in two stages. First, the banking agencies branded these disfavored industries “high risk” because of their supposed negative “reputation” in their communities. The agencies then sent federal regulators to meet with bank executives behind closed doors and to pressure them to deny companies in these industries “access to the banking and payments networks that every business needs to survive.”42 The regulators threatened the banks with extended examinations, punitive audits, and other harsh regulatory measures or, even worse, “a potentially ruinous lawsuit by the Department of Justice.”43 The regulators’ back-room campaign of regulatory intimidation has had its intended effect: banks have been strong-armed into shutting their doors to “a wide array of lawful businesses and individuals,” many of which have gone out of business as a result, precisely as the agencies had intended. And the implications of Operation Choke Point are stark and unsettling.

A. The Government’s Plan To “Choke Off” Legitimate Industries From Banking Services

Banks and other financial institutions, perhaps unique among American industries, operate in a world where government regulation and supervision is as pervasive as oxygen. As one prominent scholar recognized nearly five decades ago, “[t]he regulation of national banks has been characterized as being more intensive than the regulation of any other industry, . . . [for] it extends to all major steps in the establishment and development of a national bank, including not only entry into business, changes in status, consolidations, reorganizations, but also the most intensive supervision of operations.”44 Indeed, the U.S. Supreme Court, in an early case, observed that the politically unaccountable agencies that supervise our Nation’s banks “maintain virtually a day-to-day surveillance of the American banking system” through such regulatory tools as requiring “detailed periodic reports of [all banking] operations,” as well as the agencies’ “broad visitorial power” to order, for any reason or no reason at all, an “intensive” and “thorough examination of all the affairs of the bank.”45

The regulatory power of the banking agencies is not only more encompassing than in other industries, it is also less open and accountable to the public. Rather than setting rules and policy through formal, public processes, the banking agencies have long preferred to exercise their influence through informal methods of “arm-twisting,”46 such as convincing banks to “voluntarily” agree to certain “conditions” in return for the regulator’s approval of certain actions,47 and other forms of “persuasion.”48 The banking agencies, in other words, “proceed[ ] to a significant extent in shadowy, informal ways, outside of public view and, usually, without judicial review.”49

Traditionally, the banking regulators have wielded their formidable power with the aim of influencing the actions of the banks themselves. The launch of Operation Choke Point, however, marked the beginning of a new era in the history of these agencies’ regulatory reach. For Choke Point represents the effort of these agencies to leverage their dominating power over banks as a means of exercising control over the bank’s customers. In the modern economy, of course, nearly every individual or business relies upon the financial services provided by banks; it is the financial oxygen of commerce. Accordingly, this power-grab pioneered by Operation Choke Point, if successful, would give the banking regulatory agencies an authority and influence that is, quite literally, unlimited in scope.

While agency officials have worked to conceal details about Operation Choke Point, internal documents that have come to light reveal that the backroom campaign can be traced back to a November, 2012 Department of Justice internal memorandum. Because “Banks are sensitive to the risk of civil/criminal liability and regulatory action,” the 2012 memo explained, merely by “sending a letter to a senior bank executive inquiring” about “whether the bank is aware” of certain “red flag[s] of potential fraud,” the government could prompt “the bank to scrutinize immediately its relationships” with the targets of the campaign.50 And the Justice Department, the memo noted, could work closely with several other “Partner agencies,” including the Federal Deposit Insurance Corporation, the Federal Reserve, the Office of the Comptroller of the Currency, and the Consumer Financial Protection Bureau, “several of which already support” the project.51 Even at this early planning stage, it was plain that the main attraction of the operation, within the Justice Department, was that it could “overcome existing limitations” of proceeding through ordinary, legal channels.

Operation Choke Point, as previously noted, proceeded in two stages. The agencies that regulate banks have oversight authority to ensure that banks protect their “safety and soundness” by carefully managing a variety of risks, including their so-called “reputation risk.” As customarily understood in the banking industry and as previously defined by all three banking agencies, “reputation risk” reflected “the potential that negative publicity regarding an institution’s business practices, whether true or not, will cause a decline in the customer base, costly litigation, or revenue reductions.”52 While a bank had to protect its own reputation for fair and lawful business practices, it did not have to pass judgment on the reputations of its customers. In November 2008, however, the banking agencies departed from this settled understanding, expanding the concept of “reputation risk” to encompass risks to a depository institution that supposedly could arise from a customer’s reputation.53

This new understanding—adopted through informal guidance documents without notice-and-comment rulemaking or statutory authorization—offers no objective regulatory criteria for reliably ascertaining and measuring a bank customer’s public reputation or popularity or for distinguishing between responsible, law-abiding bank customers and bank customers that engage in fraudulent or otherwise wrongful financial practices.54 It thus equips the banking regulators with an inherently subjective, easily manipulated fulcrum with which to move banks to choke off legitimate businesses that the regulators believe are (or should be) disfavored by the public.

In 2011, the FDIC issued a list of 30 industries, including such lawful businesses as payday lenders, coin dealers, firearm and ammunition sellers, and credit repair services, that it deemed “high risk” and that could thus taint a banks’ reputation by association if it chose to serve them.55 The scope of the regulatory agencies’ powers was thus critically redefined, reaching not only the reputation of the banks but also the reputation of their customers.

With the legal hook in place, the Justice Department and its allies in the banking agencies moved to stage two of their campaign to “choke off” disfavored industries’ access to ordinary banking services. Bank examiners began to go bank-to-bank and demand that the accounts of specific customers be closed as too “risky.” In the back rooms of banks around the country, agency officials warned banks that continuing to serve payday lenders and other disfavored customers would result in harsh consequences. As one examiner reportedly told a banker who initially resisted pressure to terminate the account of a payday lender: “I don’t like this product and I don’t believe it has any place in our financial system. Your decision to move forward will result in an immediate unplanned audit of your entire bank.”56 And as a report by the FDIC’s Office of the Inspector General details, one bank was subjected to a back-room campaign of threats of retaliation and repeated examinations for a full eight months solely because it had a single payday lender as a customer.57 The agencies’ message could not be clearer: If your bank refuses to turn against customers we don’t like, we will turn against your bank.

An internal status report issued after Operation Choke Point had been in place for six months reveals Department of Justice officials openly celebrating the brutal effectiveness of their back-room campaign against disfavored customers of regulated banks.58 “[W]e have observed a dramatic shift in the banking industry,” the report notes. “All signs indicate that Operation Choke Point is having an unprecedented effect on banks” and creating an “unparalleled level of deterrence”—forcing banks, out of fear, to “scrutinize[]” and terminate “potentially problematic relationships.” The Justice Department characterized the terminations “positive conduct,” even though it recognized “the possibility that banks may have therefore decided to stop doing business with legitimate [companies].”

B. Operation Choke Point’s Scope

As these internal documents show, Operation Choke Point’s scope is expansive and its effect on its targeted victims has been cruel and uncompromising. The campaign has had perhaps the greatest effect in the payday lending industry—the first name on the government’s blacklist.

A payday loan is simply an advance on the borrower’s paycheck or other source of income. Payday loans provide short-term credit to over nineteen million American households. They fill a crucial financial need for people who do not have access to traditional banking services or forms of credit, and they are less costly than the informal credit systems many of these Americans would otherwise rely upon, such as overdraft protection, bounced checks, and late bill payment fees.59 Nonetheless, the bank regulators behind Operation Choke Point regarded payday lending as “unsavory”60 and “a particularly ugly practice.”61 One senior FDIC regulator, for example, insisted that the agency’s messaging always mention pornography when discussing payday lending, so as to convey a “good picture regarding the unsavory nature of the businesses at issue.”62 Another regulator frankly stated that he “literally can not stand pay day lending” and that he “sincerely” and “passionate[ly]” believes that payday lenders “are abusive, fundamentally wrong, hurt people, and do not deserve to be in any way associated with banking.”63 The same official later stated that payday lenders had brought “nothing good for banks,”64 and, upon learning over the holidays that one bank was terminating all of its relationships with payday lenders, emailed: “now that is something to celebrate over Thanksgiving!”65

Accordingly, these unelected regulators have used every tactic at their disposal to deprive the payday lending industry of the financial services it needs to survive. And they have been remarkably successful. Several major payday lenders have been forced out of business altogether; the ones that have survived are losing additional banking relationships day by day.

For instance, one major national payday lender, Advance America, has abruptly lost its longstanding positive banking relationships with numerous banks as a result of Operation Choke Point. Hancock Bank and Whitney Bank ended their relationships with Advance America because, in their words, they were “unable to effectively manage [the lenders’] Account(s) on a level consistent with the heightened scrutiny required by [their] regulators.” Fifth Third Bank stopped doing business with payday lenders altogether on the ground that the entire industry is “outside of [its] risk tolerance.” At least two of Advance America’s banks expressed regret and explained that the terminations were the result of pressure from the banking regulators.66 Another lender, Speedy Cash, Inc., lost a seventeen year banking relationship with Bank of America because the bank had been pressured to “exit[ ] the payday advance space.”67 And Texas-based lender Power Finance lost a longstanding relationship with Business Bank of Texas even though the bank had, after extensive due diligence, concluded that its relationship with the payday lender posed no risk to its reputation. Nonetheless, the bank has reported that officials at the OCC left it with no choice but to cease servicing payday lenders like Power Finance.68

Operation Choke Point has also caused severe damage to many firearm and ammunition retailers—another lawful industry that the regulators have sought to kill off. Numerous local and small firearms or ammunition dealers have “been systematically denied access to the financial system” solely because of “their participation in an industry deemed ‘high risk’ by federal regulators.”69 For example, Powderhorn Outfitters, a sporting goods store in Hyannis, Massachusetts, found its longstanding account with TD Bank terminated in 2014 because of its “involvement in firearms sales.”70 A South Carolina firearms dealer similarly had its account terminated by SunTrust Bank for engaging in “a prohibited business type.”71 And as a House Committee report details, the FDIC pressured several banks under its regulatory thumb to enter “memorandums of understanding” that “variously ‘prohibit’ payment processing for firearms merchants, characterize loans to firearms dealers as ‘undesirable,’ and generally subject firearms and ammunition merchants to significantly higher due diligence standards.”72

Many other lawful industries have been affected by the agencies’ intimidation campaign, as well, including coin dealers and firework vendors. For example, in a 2014 article, the Executive Director of the Professional Numismatists Guild warned that Operation Choke Point “has the potential to shut down every coin dealer . . . in the United States as well as curtail business by overseas dealers who use US-based banks” by “pressuring banks and other financial institutions to close your accounts.”73 He lamented that “[t]he concept of innocent until proven guilty apparently no longer applies to professional numismatists.”74 Many tobacco retailers have also lost critical banking relationships as a result of Operation Choke Point,75 prompting a leading industry association to issue an “extremely urgent alert” warning members that they are being targeted based on “political reasons.”76

C. The Implications of Operation Choke Point

Operation Choke Point, if it is not checked, will surely spread beyond the specific industries that have been targeted so far. A business—every business—needs access to the basic financial services provided by banks in order to survive. And the potential for regulatory abuse inherent in the regulators’ subjective and pliant notion of “reputation risk” is patent on its face. As the Chair of the House Committee on Financial Services recently warned, this vague and subjective notion

could ostensibly be invoked to compel a depository institution to sever a customer relationship with a small business operating in accordance with all applicable laws and regulations but whose industry is deemed ‘reputationally risky’ for no other reason than that it has been the subject of unflattering press coverage, or that certain Executive Branch agencies disapprove of its business model.77

By pressuring the banks to deny basic services to lawful businesses based on reputation risk, the government is thus able effectively to target and ultimately destroy law-abiding companies or even entire lawful industries without any evidence that the businesses themselves have engaged in any wrongdoing. And the government is able to accomplish this result in a way that entirely avoids the checks and balances that it would have to navigate if it acted instead through ordinary legal channels. Indeed, the Justice Department’s inaugural memo on Operation Choke Point recognized this as the main benefit of proceeding extra-legally rather than through “a conventional approach.”78

Precisely because this back-room exercise of regulatory coercion can be used against any legitimate industry, it enables the government to pick “good” and “bad” lines of business—without any legal or political scrutiny whatsoever. While the Obama administration sought to end the businesses that it found politically offensive, there is nothing stopping other administrations from targeting a very different set of companies that they “literally can not stand”—marijuana distributors, say, or renewable energy companies, or abortion providers. When government officials possess the power to cut any company off from the modern financial and banking system based on nothing more than the whim of the people currently in power, no business or trade is safe.

Our constitutional system was founded on a different vision—a vision of an open government accountable to the people, not government by backroom, regulatory coercion. Under that system, a government official cannot put a company out of business—even if he finds the company “unsavory”—without going through some regular legal process: passing legislation, issuing regulatory rules in the open, or bringing formal legal action against it for wrongdoing. And each of these ordinary legal channels is limited in such a way that multiple government officials with competing perspectives and institutional interests—Congress and the President; a prosecutor and a jury—must all agree before the coercive force of the government is brought into action. The price of these checks and balances, of course, is that law-abiding companies deemed unsavory by government officials cannot be put out of business “[i]n a short time and with relatively few resources” spent by the Government.79 But the benefit is a government of laws rather than men.

IV. The CFPB’s Shakedown of Ally Financial

When Congress created the Consumer Financial Protection Bureau (CFPB), it vested the Agency’s lone Director with “enormous power over American business[.]”80 In particular, Congress empowered the CFPB to “unilaterally enforce[] 19 federal consumer protection statutes, covering everything from home finance to student loans to credit cards to banking practices.”81 One of these statutes, known as the Equal Credit Opportunity Act (ECOA), makes it unlawful for creditors to discriminate on the basis of race and other factors.82

Congress, however, exempted one small corner of the U.S. economy from the CFPB’s purview: car dealers. Under Dodd-Frank, the CFPB “may not exercise any rulemaking, supervisory, enforcement or any other authority . . . over a motor vehicle dealer.”83 Instead, this power belongs to the Federal Reserve and other agencies.84

The law, however, is no impediment to an unaccountable agency that has set its sights on disfavored industries. By design, the CFPB is wholly independent from both Congress and the President.85 This lack of political checks gives the CFPB’s director free reign to pursue his natural interest “in expanding the power, influence and budgets of [his] agency.”86 Indeed, the CFPB Director is so independent that he answers questions by members of Congress about a $216 million splurge with the retort, “[w]hy does that matter to you?”87

Only one month after being (illegally)88 appointed without being confirmed by the Senate, the CFPB’s Director set his sights on car dealer loan price “markups,” creating an “Auto Finance Discrimination Working Group” within the CFPB to investigate this practice.89

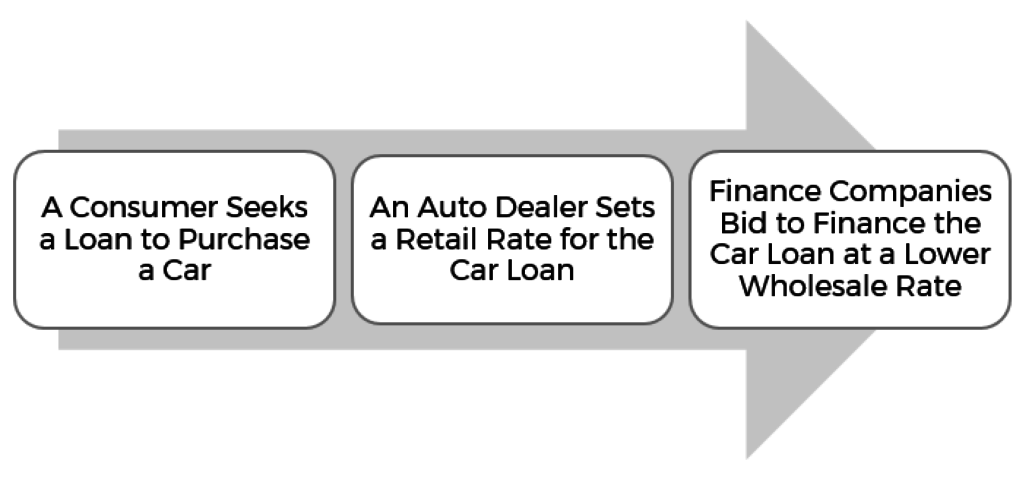

Price markups are common—indeed essential—to retail industries.90 The auto loan market is no different. Most car purchases are financed through so-called indirect auto loans.91 In such transactions, car dealers function as retailers for the loan, originating the loans and setting the rates paid by the car purchaser.92 Finance companies (indirect auto lenders) then compete to buy the loans by accepting lower interest rates on them than the dealer accepts from the purchasers.93 When the indirect loan market functions properly, all parties benefit: finance companies profit from the interest generated by the loans, dealers profit from the spread between the two rates (the dealer “markup”), and purchasers benefit from the resulting convenience and expanded access to credit.94

Indirect Auto Loans

In the CFPB’s view, however, the retail market was rigged. CFPB staff believed that car dealer markups were too high.95 Accordingly, the CFPB set out on a war path to squeeze—or entirely eliminate—markups by ending the car dealers’ retail rate-setting discretion.96

To achieve this goal, which Congress had prohibited, the CFPB came up with a plan of evasion. Instead of going directly after the car dealers, the CFPB used scare tactics to enlist indirect auto lenders in its effort to change the car dealers’ retail practices.97 In essence, the CFPB planned to coerce vulnerable indirect auto lenders into punitive discrimination settlements under ECOA to pressure the industry into re-negotiating their contracts with auto dealers to reduce or eliminate car dealers’ retail discretion.98

One of the third-party lenders targeted by the CFPB was Ally Financial.99 On November 7, 2013, the CFPB referred the matter to DOJ.100 By December of 2013, the parties had reached a deal, filing a settlement for court approval.101

The settlement severely punished Ally for its alleged violations of ECOA. First, under the settlement, Ally was required to develop a “compliance plan” that forced it to, among other things: (1) “limit[] the . . . spread between” its rate and the dealers’ rates; and (2) periodically identify and remunerate racial disparities in its pricing data, using the CFPB’s chosen methodology for assessing discrimination.102 Second, Ally was required to pay $80 million into a fund to compensate its purported victims.103 Third, Ally was required to pay $18 million into the CFPB’s Civil Penalty Fund.104 As DOJ boasted in its press release, the settlement was “the largest auto loan discrimination settlement in history.”105

Given the highly punitive terms of the settlement, one would think that there was clear evidence that Ally was engaged in racial profiling. But there was no evidence of racial profiling. Indeed, Ally did not know the race of its customers, because by regulation, car purchasers’ credit applications do not include information about race, national origin, or any other protected characteristics.106 Ally was being punished, not for its own discrimination, but rather, for its alleged acquiescence to the car dealers’ allegedly discriminatory practices.107

To hold Ally liable for the car dealers’ practices, the CFPB relied on a dubious legal premise. The CFPB contended that Ally could be held liable under a “disparate impact” theory.108 Essentially, this means that Ally could be held liable if its policies caused racial minorities to pay more than similarly-situated non-minorities, even if Ally did not discriminate.109 But laws that authorize disparate impact do so because they have language directed to the consequence of discrimination (for example “otherwise adversely affect” protected minorities), and “ECOA contains no such language.”110

In addition to pursuing a dubious legal theory, CFPB relied on a flawed statistical methodology to assess racial disparities. The methodology uses zip code and last name proxies for race.111 Among its many failings, the CFPB’s methodology failed to control for credit scores, one of the few factors that auto lenders do take into account when making decisions.112 The resulting race predictions are wildly inaccurate, as even the CFPB has internally acknowledged.113

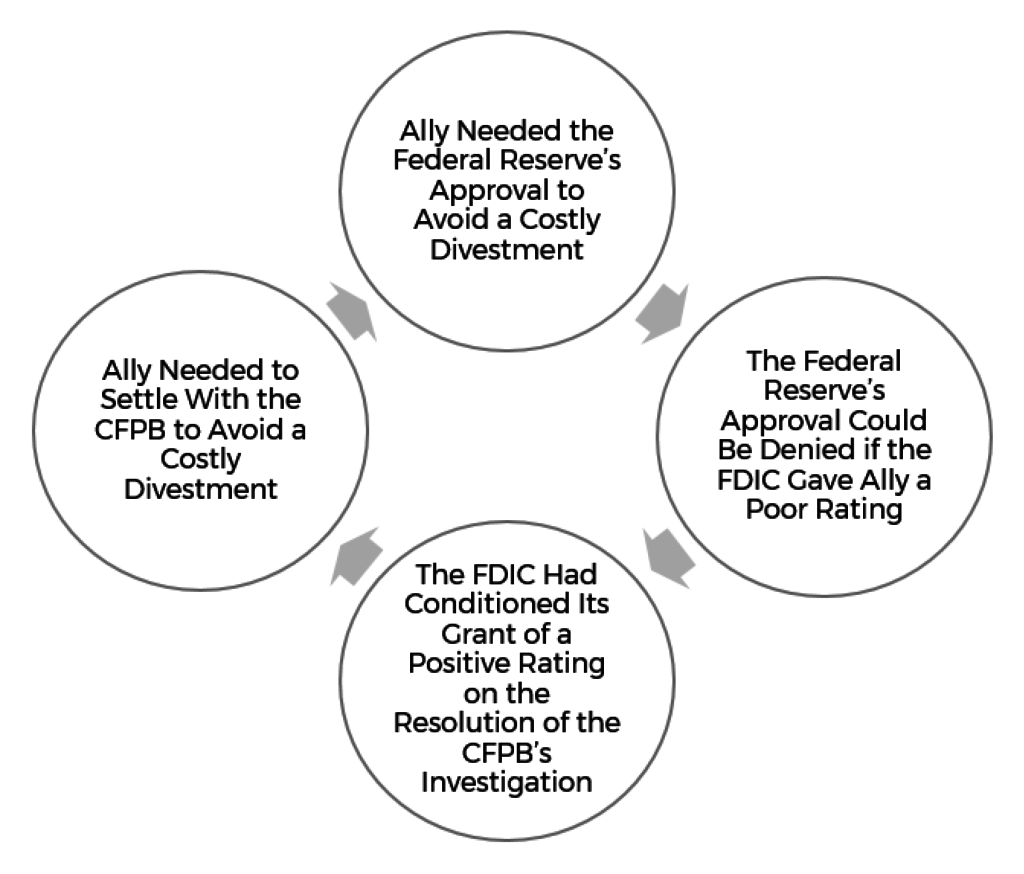

In short, there was no good reason for Ally to capitulate to the CFPB’s punitive demands. So why did Ally capitulate? As demonstrated by records collected by the House Financial Services Committee, CFPB used its external leverage over Ally to strong-arm the company into submission. In particular, during the relevant time period, “Ally had an application pending before the Federal Reserve to change its status [from a bank holding company] to a financial holding company.” If “the Federal Reserve did not approve the [application] by December 24, 2013, Ally would have to divest its insurance and used-car remarketing operations” to avoid violating banking rules.114 At the same time, the FDIC was reviewing Ally’s lending activities, “and a poor rating by the FDIC could have precluded” the Federal Reserve’s approval of Ally’s application.115 The FDIC, however, had deliberately conditioned the grant of a positive rating on the resolution of the CFPB’s investigation.116 Thus, if Ally decided to resist the CFPB in court, it faced the risk of a disastrous corporate divestment.

The CFPB’s Leverage Over Ally

There is strong documentary evidence that the CFPB coordinated with the FDIC and the Federal Reserve to strong-arm Ally into a settlement.117 Conspicuously, the CFPB’s Director sits on the Board of the FDIC.118 It is no coincidence that on the same day that the settlement agreement was filed in court, the Federal Reserve granted Ally’s application.119

It is difficult to quantify the economic damage caused by the CFPB’s abusive conduct toward Ally. According to one report, the CFPB’s broader enforcement campaign against indirect auto lenders has resulted in higher costs for consumers.120 As an added bonus, because the CFPB has decided to distribute the settlement funds using its flawed statistical methodology, a large portion of Ally’s payments under the settlement will likely go to non-minorities that could not have possibly been harmed.121

Ally was being punished, not for its own discrimination, but rather, for its alleged acquiescence to the car dealers’ allegedly discriminatory practices.

V. The Car Deal That Automakers Could Not Refuse

Over the course of eight years, the Obama Administration adopted two greenhouse gas (GHG) and fuel economy standards applicable to cars and light-trucks. The first set of standards, issued in 2010, apply to vehicles produced from 2012 to 2016.122 The second set of standards, issued in 2012, apply to vehicles produced from 2017 to 2025.123

On both occasions, the standards were finalized after “historic agreements” negotiated in secret by key players within the Administration, automakers, and state regulators (primarily California).124 On both occasions, automakers agreed to surrender their right to pursue viable legal challenges against federal and state fuel economy regulations.125 In exchange, California agreed to deem compliance with the national GHG emission standards as sufficient to comply with California’s standards.126

Jodi Freeman, a former White House advisor who participated in the negotiations leading to the first “car deal,” contends that the deal “benefited the auto industry by harmonizing a patchwork of inconsistent regulations, and removing . . . the threat that California would implement its separate and more stringent standards.”127 Freeman portrays the deal as a laudable and rare form of industry cooperation, done “not under a consent decree . . . but voluntarily.”128

That is a highly sanitized version of history, written by the victors. It ignores that on both occasions, the Administration deliberately encouraged California to establish a two-car regulatory patchwork, and then—together with California—used the enticement of a single national standard to strip automakers of legal rights.129 The automakers’ gain from the car deal was not unlike the insurance gained by shopkeepers who buy into a protection racket. Although the commitments look altruistic on their face, it is not difficult to see why automakers caved in: quite simply, the Administration made them an offer that they “could not refuse.”130

Until President Obama came into office, EPA had rejected California’s attempt to regulate motor vehicle GHG emissions.131 Because GHG emissions are not pollutants particularly affecting California, EPA had determined that California had failed to demonstrate the “extraordinary circumstances” required by law to regulate GHG emissions.132 After a change in Administration, EPA swiftly changed course, allowing California to regulate GHG emissions.133

It was evident that this would result in a balkanized vehicle market, imposing inconsistent and costly requirements on automakers.134 At the time, approximately 13 states—accounting for 40% of the nation’s auto market—had decided to opt into California’s standards.135 On the other hand, California’s regulations would do little to curb national GHG emissions: under the existing federal fuel economy program, automakers could offset sales of fuel efficient vehicles in California states by selling gas guzzlers in other states.136 Thus, allowing California to regulate GHG emissions threatened to impose severe costs on automakers in exchange for little or no discernible benefit. Given this reality, EPA’s decision cannot be explained except as a deliberate, strategic step in a scheme to coopt automakers into accepting the national program of the Administration’s choice.

The Administration also used its bailout authority to threaten domestic automakers into submission.137 Shortly after EPA announced its intent to revisit the California waiver, in March of 2009, President Obama “rejected” Chrysler and GM’s proposed business viability plans, giving the auto companies just weeks “to devise a more thorough restructuring and thereby qualify for more U.S. government aid.”138 This temporary rejection gave the Administration the leverage it needed to gain GM and Chrysler’s support for the Administration’s fuel economy plans, giving EPA and the Administration the upper hand in its negotiations.139 The President could credibly threaten to hold onto taxpayer funds unless GM and Chrysler agreed to his demands.

During the weeks leading up to the announcement of the first car deal in May of 2009, and the day following that announcement, GM received at least $200 million in federal grants to develop electric vehicles.140 And just three weeks later, “the Administration reached agreements to bail out” GM and Chrysler.141

As a result of this two-pronged approach, “the Administration could say, the domestic auto industry not only would survive, but would also start down the path of making cleaner cars.”142 Unfortunately, the bailouts yielded an ultimate net loss of $9.2 billion to the taxpayer.143 And ironically, Chrysler and General Motors returned to profitability by selling the light trucks and large cars that their customers want, not the compact cars favored by the Administration.144

Thus, allowing California to regulate GHG emissions threatened to impose severe costs on automakers in exchange for little or no discernible benefit.

VI. The CFPB’s Abusive Use of Civil Penalties Against PHH

When Congress created the Consumer Financial Protection Bureau (CFPB), it vested the Agency’s lone Director with “enormous power over American business[.]”145 In particular, Congress empowered the CFPB to “unilaterally enforce[] 19 federal consumer protection statutes, covering everything from home finance to student loans to credit cards to banking practices.”146 One of these statutes, known as the Real Estate Settlement Procedures Act (RESPA), prohibits real estate companies from paying “kickbacks” in exchange for referrals.147

Recognizing “that an aggressive agency” could use RESPA to sweep too broadly, Congress provided a safe harbor for services provided at “reasonable market value.”148 This safe harbor had been authoritatively interpreted to permit so-called captive mortgage reinsurance arrangements.149 In such an arrangement, a mortgage lender refers a borrower to a mortgage insurer, which insures the mortgage lender against the risk of default. The mortgage insurer then pays part of the premium to a reinsurer affiliated with the lender.150 Recognizing that, in a competitive market, lenders and insurers benefit from spreading mortgage risks, the Department of Housing and Urban Development (HUD) had repeatedly approved the practice.151 Relying on HUD’s pronouncements, PHH, a mortgage lender, entered into captive reinsurance arrangements for almost two decades.152

But in 2011, the CFPB arrived on the scene.153 The CFPB takes a dim view of captive reinsurance. In the Agency’s view, these arrangements are scams, even though the details are disclosed fully and borrowers are free to shop elsewhere for insurance.154

The CFPB’s opposition to captive reinsurance is consistent with its aggressive use of its new powers155 But one would expect an agency of the federal government to at least give the real estate industry fair notice of a change in policy before banning these arrangements.

The CFPB’s Director, however, has demonstrated a preference for expanding his power (and re-fashioning entire industries) through enforcement actions.156 This wrecking-ball approach has worked reasonably well for the Agency, but very badly for the regulated community: all lenders threatened by the CFPB’s enforcement of RESPA settled on terms favorable to the CFPB.157

All except PHH.

In 2014, the CFPB sued PHH for allegedly violating RESPA’s prohibition against kickbacks.158 The case was heard by an administrative law judge.159 The judge found PHH liable for violating RESPA’s prohibition against kickbacks and recommended that it pay $6.4 million to disgorge its reinsurance profits.160 Still, PHH did not settle.

Instead, PHH appealed the decision to the CFPB’s Director, who conveniently sits as both judge and prosecutor in the CFPB’s enforcement cases. Notably, this was “the first administrative proceeding to give rise to an appeal” in more than five years of the Bureau’s existence.161 Nobody else had resisted.

In his written opinion, the CFPB Director set out to make sure no one else would dare resist again. He ordered PHH to disgorge a whopping $109.2 million of premium payments from its captive reinsurance business—approximately 17 times the figure ordered by the administrative law judge.162 The Director reached this outcome by announcing a “newly minted” interpretation of RESPA that banned PHH from entering into captive reinsurance arrangements in the future conduct and retroactively punished PHH for its past conduct.163 The Director further inflated the penalty by: (1) declaring that the ordinary statute of limitations did not apply to any of his decisions;164 (2) finding that every premium payment (as opposed to a contract for payment) was a RESPA violation; and (3) refusing to offset PHH’s costs from the disgorgement award.165

Fortunately, PHH was able to appeal to an actual court of law. The Court of Appeals for the D.C. Circuit held that the Director had badly misinterpreted the law on all counts, and in doing so, had violated bedrock principles of due process.166 The Court also held that the CFPB’s unaccountable structure violated the constitutional separation of powers, striking down the Director’s statutory protection against being fired by the President.167

The Court of Appeals for the D.C. Circuit held that the Director had badly misinterpreted the law on all counts, and in doing so, had violated bedrock principles of due process.

VII. Volkswagen ZEV Settlement Agreement

In 2016, EPA sued Volkswagen for installing devices designed to cheat EPA’s emissions tests on roughly 580,000 vehicles sold in the United States.169 In a striking example of regulatory failure, VW had for years illegally sold cars “with emission control systems that satisfied regulators’ mandatory emission tests . . . but that emitted forty times more pollutants than allowed by law when driven on the road.”170

In a June 2016 partial court settlement, VW agreed to partially settle EPA’s lawsuit. As part of that settlement, VW agreed to “direct” $2 billion to “investments over a 10-year period to support increased use” of so-called “Zero Emission Vehicles” (ZEVs): an acronym for the electric cars favored by EPA.171 In particular, VW agreed to “promot[e] and advanc[e] the use and availability of ZEVs” by, among other things, investing in charging stations and sponsoring ZEV education and awareness projects.172

There is no reason to think that VW is making these ZEV-related investments “out of the goodness of [its] heart.”173 If investing billions of dollars to promote ZEVs was in VW’s interest, it would make these investments without EPA’s prompting. VW is making these investments only because its illegal conduct exposed it to effectively unlimited liability—potentially $68 billion in penalties, or more than 90% of VW’s $73 billion market capitalization at the time of settlement.174 Under these circumstances, VW was clearly compelled to agree to EPA’s demands.

The settlement’s ZEV-related investment provisions have no logical relation to VW’s violations. EPA’s ostensible rationale for the ZEV-related investment provisions is that they “address the adverse environmental impacts arising from consumers’ purchases of the” offending vehicles.175 But these impacts are already addressed by VW’s agreement to create a $2.7 billion Environmental Mitigation Trust Fund to “fully mitigate the total, lifetime excess . . . emissions” from VW’s offending vehicles.176 On its face, therefore, the ZEV provisions do not mitigate any environmental harm.

Instead, the VW settlement is an egregious example of self-appropriation through litigation. The ZEV provisions augment EPA’s appropriations by funding unenacted presidential policy preferences that Congress has implicitly but clearly rejected.

Electrifying the nation’s automobile fleet was an early priority of the Obama Administration.177 In 2011, President Obama requested $300 million from Congress to “catalyze electric vehicle deployment.”178 In 2016, President Obama also asked Congress to impose a $10 per barrel tax on oil to finance ZEV-related investments through his “21st Century Transportation Initiative.”179

Congress, however, never supported the President’s ZEV-related infrastructure plans. Instead, in the 2015 FAST Act, Congress directed the Secretary of Transportation to establish “electric vehicle charging and hydrogen, propane, and natural gas fueling corridors” throughout the nation.180 Rather than make direct investments in infrastructure, the FAST Act directs the Secretary of Transportation to “identify the near- and long-term need for, and location of” fueling and charging infrastructure “at strategic locations along major national highways.”181

The settlement’s ZEV-related investment provisions represent a clear evasion of Congress’ decision to reject the President’s ZEV-related infrastructure plan and to map out a different course for federal involvement in alternative fuels infrastructure development.

Indeed, not only does the VW settlement promote policies that Congress has rejected; it creates a de facto ten-year public infrastructure program subject to no checks by the other branches of government. The ZEV-related provisions are more akin to a centrally-planned infrastructure program, with VW acting as a conscripted contractor, than an environmental mitigation plan. The settlement’s provisions control the details of VW’s investment decisions, and give EPA the power to review and veto VW’s investment choices.182 In practice, this allows EPA to substitute its own preferences for VW’s business judgment. EPA’s frequently asked questions sheet seeks to clarify that the ZEV-related investments are “not a government program[.]”183 But the only difference between the settlement’s ZEV provisions and a “government program” is that in the case of the settlement, Congress has authorized no funds, and EPA has complied with none of the laws that typically apply to public infrastructure projects.

The settlement’s violation of the separation of powers comes at a great public cost. In spite of their much vaunted expertise, executive agencies like EPA tend to suffer from tunnel vision and random agenda selection.184 Congressional control over agency funds helps to moderate and check these tendencies.185 The legal requirement that agencies engage in reasoned decision-making when making rules that impose costs provides an additional check.186 By empowering EPA to direct private funds into areas—such as vehicle infrastructure and education—that are outside of EPA’s area of expertise, in defiance of Congress and without making record findings demonstrating that the funds will in fact mitigate pollution, the settlement gives free reign to EPA’s worst bureaucratic tendencies without any guaranteed environmental return. That is not a sensible way of making use of limited resources or promoting innovation in the transportation sector.

By empowering EPA to direct private funds into areas—such as vehicle infrastructure and education—that are outside of EPA’s area of expertise, in defiance of Congress and without making record findings demonstrating that the funds will in fact mitigate pollution, the settlement gives free reign to EPA’s worst bureaucratic tendencies without any guaranteed environmental return.

Footnotes

1 Bebo v. Sec. and Exch. Comm’n, 799 F.3d 765, 768 (7th Cir. 2015); Urska Velikonja, Securities Settlements in the Shadows, 126 Yale L.J. F. 124 (2016), https://ssrn.com/abstract=2838558

2 Dodd-Frank Wall Street Reform and Consumer Protection Act, Pub. L. No. 111-203, § 929P, 124 Stat. 1376 (2010).

3 According to data collected and published in the Yale Law Journal Forum, “between FY 2007 and FY 2012, the SEC filed around 200 settlements per year in court.” Velikonja, supra note 1, at 130. Following the change in the law, the number of settled proceedings in federal court steadily dropped and, in FY 2015, “the SEC filed only 83 settlements in court, compared with 419 settlements filed in administrative proceedings.” Id.

4 Tyler L. Spunaugle, The SEC’s Increased Use of Administrative Proceedings: Increased Efficiency or Unconstitutional Expansion of Agency Power?, 34 Rev. Banking & Fin. L. 406, 412 (2015).

5 Hill v. Sec. and Exch. Comm’n, 825 F.3d 1236, 1238 (11th Cir. 2016).

6 Id.

7 Id.

8 See Press Release, Securities and Exchange Commission, SEC Adopts Amendments to Rules of Practice for Administrative Proceedings (July 1, 2016), https://www.sec.gov/news/pressrelease/2016-142.html

9 Hill, 825 F.3d at 1238.

10 Bandimere v. Sec. and Exch. Comm’n, No. 15-9586, 2016 WL 7439007, at *7 (10th Cir. Dec. 27, 2016).

11 Id. at * 10.

12 In contrast to the Tenth Circuit, a panel of three judges in the D.C. Circuit initially determined that the appointments of ALJs were not unconstitutional. Raymond J. Lucia Cos., Inc. v. Sec. and Exch. Comm’n, 832 F.3d 277, 289 (D.C. Cir. 2016). However, the D.C. Circuit has now vacated that decision, and an en banc oral argument on the case was heard on May 24, 2017. Minutes of Oral Argument, Raymond J. Lucia Cos., Inc. v. Sec. and Exch. Comm’n, No. 15-1345 (D.C. Cir. May 24, 2017).

13 The Honorable Jed S. Rakoff, PLI Securities Regulation Institute Keynote Address: Is The S.E.C. Becoming A Law Unto Itself?, Law 360 (Nov. 5, 2014), http://assets.law360news.com/0593000/593644/Sec.Reg.Inst.final.pdf

14 See, e.g., Andrew Ceresney, Securities and Exchange Commission, Remarks to the American Bar Association’s Business Law Section Fall Meeting (Nov. 21, 2014), https://www.sec.gov/news/speech/2014-spch112114ac#_ftn12

15 48 C.F.R. § 9.104-1 (2011) (setting forth requirements for present responsibility, including the requirement that a contractor have “a satisfactory record of integrity and business ethics”); 48 C.F.R. § 9.406-4 (2014) (setting forth the period of debarment).

16 48 C.F.R. § 9.406-2 (2015); see also id. (also permitting debarment “based on any other cause of so serious or compelling a nature that it affects the present responsibility of the contractor or subcontractor”).

17 48 C.F.R. § 9.402(b) (2014) (setting forth the policy behind debarment and suspension).

18 Warren Bianchi, Equality in Exclusion: Empowering Individuals in the Suspension and Debarment System, 45 Pub. Cont. L.J. 79, 89 (2015) (discussing collateral consequences to debarment such as “damage to reputation and goodwill, lost revenue, the revocation of security clearance or specialty license, the contraction of credit, denial of loans, and the denial of commercial contracts”).

19 United States v. WakeMed, No. 5:12-CR-398-BO, 2013 WL 501784, at *1 (E.D.N.C. Feb. 8, 2013).

20 Anne Blythe & Joseph Neff, WakeMed Admits to False Medicare Billing in $8m Settlement, News & Observer (Dec. 19, 2012), 2012 WLNR 27392696 (Westlaw).

21 Deferred Prosecution Agreement at ¶¶ 10(a), (e), United States v. WakeMed, 5:12-cr-00398-BO (E.D.N.C. Dec. 19, 2012), ECF No. 18.

22 Id. at ¶ 10(e).

23 Id. at ¶ 10.

24 WakeMed, 2013 WL 501784, at *1.

25 Id.

26 Id.

27 Deferred Prosecution Agreement, supra note 7, at ¶ 9.

28 Blythe, supra note 6, at 1.

29 WakeMed, 2013 WL 501784, at *2.

30 Deferred Prosecution Agreement, supra note 8, at ¶ 20.

31 Complaint, United States ex rel. Brunson v. Bechtel Nat’l, Inc., No. 2:13-cv-05013-EFS (E.D. Wash. Feb. 4, 2013), ECF No. 1.

32 Id. at 18; Gene Johnson & Phuong Le, Feds: Hanford Contractors to Pay $125 Million Settlement, U.S. News & World Report (Nov. 23, 2016), http://www.usnews.com/news/business/articles/2016-11-23/feds-hanford-contractors-to-pay-125-million-settlement

33 Complaint, supra note 17, at ¶¶ 155-58; 227-30.

34 Id. at ¶¶ 271-90.

35 Kat Greene, US, Nuke Site Contractors Reach $125M Deal in FCA Suit, Law 360 (Nov. 23, 2016), https://www.law360.com/articles/866018/us-nuke-site-contractors-reach-125m-deal-in-fca-suit

36 Id.

37 Press Release, Bechtel National, Inc. Resolves Civil Lawsuit Related to Hanford Waste Treatment Plant Project (Nov. 23, 2016), http://www.bechtel.com/newsroom/releases/2016/11/bechtel-resolves-lawsuit-wtp/

38 Press Release, Department of Labor, U.S. Department of Labor Sues Silicon Valley Tech Company for Discriminating Against Asian Job Applicants (Sept. 26, 2016), https://www.dol.gov/newsroom/releases/ofccp/ofccp20160926

39 Complaint for Violations of Executive Order 11246 at ¶ 11, OFCCP v. Palantir Techs., Inc., (Dep’t of Labor Sept. 26, 2016), https://www.dol.gov/sites/default/files/newsroom/newsreleases/OFCCP20160926_0.pdf

40 Id. at ¶ 14(B)-(C).

41 Lizette Chapman, Palantir Settles Discrimination Complaint with U.S. Labor Agency, Bloomberg (Apr. 25, 2017), https://www.bloomberg.com/news/articles/2017-04-25/palantir-settles-discrimination-complaint-with-u-s-labor-agency

42 Staff of H. Comm. on Oversight & Gov’t Reform, 113th Cong., Rep. on the Dep’t of Justice’s ‘Operation Choke Point’: Illegally Choking Off Legitimate Businesses? 5 (Comm. Print 2014).

43 Id.

44 1 K. Davis, Administrative Law Treatise 247 (1958).

45 United States v. Philadelphia Nat. Bank, 374 U.S. 321, 329 (1963).

46 Lars Noah, Administrative Arm-Twisting in the Shadow of Congressional Delegations of Authority, 1997 Wis. L. Rev. 873, 895 (1997).

47 Alfred C. Aman Jr., Bargaining for Justice: An Examination of the Use and Limits of Conditions by the Federal Reserve Board, 74 Iowa L. Rev. 837, 893 (1989).

48 United States v. Gaubert, 499 U.S. 315, 333 (1991).

49 Michael P. Malloy, Balancing Public Confidence and Confidentiality: Adjudication Practices and Procedures of the Federal Bank Regulatory Agencies, 61 Temp. L. Rev. 723, 725 (1988).

50 Memorandum from Joel M. Sweet to Stuart F. Delery at 2–3 (Nov. 5, 2012) (emphasis added), available at H.R. Comm. on Oversight & Gov. Reform Report: The Department of Justice’s “Operation Choke Point,” Appendix at HOGR-3PPP000016 (May 29, 2014), https://goo.gl/Ny4WQ7 (“House Report Appendix”).

51 Id. at 3.

52 FDIC, Foreign-Based Third-Party Service Providers: Guidance on Managing Risks in These Outsourcing Relationships, FIL-52-2006 (June 21, 2006).

53 “Guidance on Payment Processor Relationships.” FDIC, Financial Institution Letter: Guidance on Payment Processor Relationships, FIL-127-2008 (Nov. 7, 2008), https://goo.gl/2wpRhe

54 Indeed, as it has been redefined, “reputation risk” now comprises nothing more than the “risk” that arises when a bank does business with a law-abiding customer who regulators believe is (or, in their view, should be) unpopular. The banking regulators’ guidance documents expressly distinguish “reputation risk” from “compliance risk,” defining the latter as the risk to the bank of doing business with customers that engage in fraudulent, deceptive, or otherwise unlawful practices. E.g., FDIC, FIL: Guidance for Managing Third Party Risk, FIL-44-2008 (June 6, 2008), http://goo.gl/6X9vQM. The risk that a bank is doing business with a customer who is breaking the law is thus fully captured within the category of compliance risk.

55 FDIC, Managing Risks in Third-Party Payment Processor Relationships, Supervisory Insights, Summer 2011. The other industries listed by the FDIC were: cable box de-scramblers, credit card schemes, dating services, debt consolidation scams, drug paraphernalia, escort services, fireworks sales, get rich products, government grants, home-based charities, life-time guarantees, life-time memberships, lottery sales, mailing lists/personal info, money transfer networks, on-line gambling, pharmaceutical sales, Ponzi schemes, pornography, pyramid-type sales, racist materials, surveillance equipment, telemarketing, tobacco sales, and travel clubs.

56 Guilty until Proven Innocent? A Study of the Propriety & Legal Authority for the Justice Department’s Operation Choke Point: Hearing Before the H. Comm. on the Judiciary, 113th Cong. 5 (July 17, 2014) (statement of Chairman Bob Goodlatte), https://goo.gl/LcXMGI

57 Office of Inspector General, Report No. AUD-15-008: The FDIC’s Role in Operation Choke Point and Supervisory Approach to Institutions that Conducted Business with Merchants Associated with High-Risk Activities at 25–27 (Sept. 2015).

58 Memorandum from Michael S. Blume, Dir., Consumer Prot. Branch of U.S. Dep’t of Justice, to Stuart F. Delery, Principal Deputy Ass’t Att’y Gen., Civil Division of the U.S. Dep’t of Justice 14 (Sept. 9, 2013).

59 A payday loan is secured by a post-dated check or pre-authorized electronic debit provided by the borrower when the loan is made. In order for this security to be effective, however, the payday lender must have access either to a bank deposit account or the Automated Clearing House network. Payday lenders therefore depend on access to traditional sources of basic financial services and credit, like banks, and it was this dependence that the agencies behind Operation Choke Point determined to exploit.

60 Email from a Counsel, Legal Division, FDIC, to Marguerite Sagatelian, Senior Counsel, Consumer Enforcement Unit, FDIC (August 28, 2013; 9:32AM), FDICHOGR00007424.

61 Email from a Counsel, Legal Division, FDIC, to Marguerite Sagatelian, Senior Counsel, Consumer Enforcement Unit, FDIC (March 9, 2013; 2:53PM), FDICHOGR00005178.

62 Staff Report of the H. Comm. on Oversight & Gov’t Reform, FDIC’s Involvement in “Operation Choke Point” at 1 (Dec. 8, 2014) (“House FDIC Report”).

63 Email from Thomas J. Dujenski, Regional Dir., Atlanta Region, FDIC, to Mark Pearce, Dir., Div. of Consumer Prot., FDIC (Nov. 26, 2012), FDICHOGR00006585.

64 Email from Thomas J. Dujenski, Regional Dir., Atlanta Region, FDIC, to Mark Pearce, Dir., Div. of Consumer Prot., FDIC (Mar. 22, 2013).

65 Email from Thomas J. Dujenski, Regional Dir., Atlanta Region, FDIC, to Mark Pearce, Dir., Div. of Consumer Prot., FDIC (Nov. 21, 2012).

66 Second Amended Complaint, CFSA v. FDIC, at 30, No. 14-953 (D.D.C. filed Sept. 25, 2015).

67 Id. at 31.

68 Declaration of Ed Lette, President & CEO, Business Bank of Texas, CFSA v. FDIC, No. 14-953 (D.D.C. filed Nov. 23, 2016).

69 House FDIC Report at 19–20.

70 Kelly Riddell, Operation Choke Point force bank to dump gun store, Wash. Times, May 28, 2014, https://goo.gl/3pSxhV

71 Jennifer Phillips, Gun, pawn shop owner says bank targeted business, Fox Carolina, Nov. 21, 2014, https://goo.gl/xwvdXL

72 House FDIC Report at 7.

73 Robert Brueggeman, Message from PNG to Member-Dealers (June 19, 2014), https://goo.gl/087L9s

74 Id.

75 Patrick Lagreid, Operation Choke Point Targets Cigar Manufacturer, Two More Retailers, HalfWheel.com (Sept. 11, 2015), https://goo.gl/7e95pC

76 International Premium Cigar & Pipe Retailers Association, Extremely Urgent Alert, Your Business May Be At Risk, https://goo.gl/jXrWBu

77 Letter from Rep. Jeb Hensarling, Chairman, H. Comm. on Fin. Servs., to Janet Yellen, Chair, The Fed. Reserve Sys. (May 22, 2014).

78 House Oversight Report at HOGR-3PPP000019.

79 House Oversight Report at HOGR-3PPP000018.

80 PHH Corp. v. CFPB, 839 F.3d 1, 7 (D.C. Cir. 2016).

81 Id.

82 15 U.S.C. § 1691(a).

83 12 U.S.C. § 5519(b)

84 Id. § 5519(c).

85 Todd Zywicki, The Consumer Financial Protection Bureau: Savior or Menace?, 81 Geo. Wash. L. Rev. 856, 875 (2013) (“the CFPB is an extremely independent agency—more so, perhaps, than another prior agency”); see also PHH Corp., 839 F.3d 1, 7 (“the [CFPB] Director enjoys more unilateral authority than any other officer in any of the three branches of the U.S. Government, other than the President”).

86 Zywicki, supra note 6, at 878.

87 https://www.youtube.com/watch?v=5IxSfJ638cs

88 Even the CFPB concedes that the Director’s initial recess appointment was unlawful. See Nat’l Bank of Big Spring v. Lew, No. CV 12-1032 (ESH), 2016 WL 3812637, at *3 & n.3 (D.D.C. July 12, 2016) (“Defendants [including CFPB] make no attempt to rebut the argument that Corday’s recess appointment was unconstitutional”).

89 Report Prepared by the Republican Staff of the Committee on Financial Services, Hon. Jeb Hensarling, U.S. House of Representatives, Unsafe at Any Bureaucracy: CFPB Junk Science and Indirect Auto Lending, at 7–8 (Nov. 24, 2015) (Republican Staff Report).

90 Even the CFPB admits this. Id. at 18 (“[T]he Bureau acknowledges internally that so-called ‘mark ups’ are a common retail practice”).

91 CFPB, Consumer Voices in Automobile Financing 6 (Jun. 2016) (“While the precise percentage of consumers who use indirect financing is not known, industry sources suggest that indirect financing accounts for a majority of all auto finance transactions”), available at http://bit.ly/2jgL0Ae

92 Republican Staff Report, supra note 10, at 15–16.

93 Id. at 16.

94 Id. at 16–18.

95 Id. at 18 (“The Bureau views the discounted wholesale rate quoted to dealers by creditors as the interest rate to which car buyers should be entitled”).

96 Id. at 46 (“[I]nternal documents reveal that the Bureau’s objective from the beginning has been to eliminate dealer discretion and dealer reserve”).

97 Assessing the Effects of Consumer Finance Regulations: Hearing Before the S. Comm. on Banking, Housing, and Urban Affairs, 114th Cong. 83 (2016) (prepared statement of Todd Zywicki) (“Lacking the authority to reach the auto dealers, the CFPB came up with a creative solution—it decided to hold the financial institutions (the indirect lenders) responsible for any alleged discriminatory lending patterns by the auto dealers themselves”), available at http://bit.ly/2jgNvCw

98 Republican Staff Report, supra note 10, at 48 (“the Bureau described this strategy as a Market-Tipping Consent Order, the purpose of which was to attempt to enter in a consent order with several auto lenders, enough to tip the market away from discriminatory practices in general, or markup more generally”) (quotations omitted).

99 In re Ally Financial, Inc., Consent Order, File No. 2013-CFPB-0010 ¶ 9 (filed Dec. 20, 2014) (hereinafter Administrative Consent Order), available at http://bit.ly/2keKT7Y